AI Raises a Big Question, but Legacy Industries Have Already Answered It

The key to understanding which software models will create the most value lies in the economics of traditional industries.

AI is throwing venture investing into turmoil. Just look at DeepSeek’s bombshell. First, "GPT wrappers" were fragile; now, it’s the models themselves under question. And while hindsight is 20/20, our job is to predict outcomes today.

Software has long been unique: high upfront development costs counterbalanced by the potential for fast growth and high margins. But AI is changing this. Traditional businesses will start to resemble software companies, operating with higher gross margins. Meanwhile, software businesses are taking on more traditional cost structures (AI compute is not de minimis like other SaaS infrastructure).

As AI-driven and legacy markets converge, we can apply the same principles to both. Some software paradigms will fade, replaced by long-standing business models. This shift reveals where value accrues—and where Grid sees the biggest opportunities.

A new framework rooted in old industries

At the most fundamental level, companies exist to solve problems for their customers.

There are three modes for solving problems. You can own the solution, using vendor’s tools to do so. You can outsource the solution to another party. Or, you can do something in between, operate alongside someone else to solve it together.

Below are examples illustrating this framework, along with market sizes to show where the most value is concentrated.

For example, if my problem is that I am hungry. I can rely on...

Grocery stores [own] – How we source food to cook ourselves. An $830B market.

Meal kits [operate] – Receive ingredients and instructions but still have to cook. A $11B market, only 1% the size of the restaurant market.

Restaurants [outsource] – Fully prepared meals. A $1.1T market. If I need to save for my retirement, I can use...

Self-directed accounts [own] – 63% of Americans invest directly

Robo-advisor [operate] – 5% of Americans use algorithms to manage investments with their input

Financial Advisors [outsource] – 35% of Americans rely on financial advisors to make and execute investment decisionsIf I need to go somewhere. I can…

Purchase a new car [own] - A $650B market for new car sales in the U.S.

Rent a car [operate] - A $65B market, where consumers drive but don’t own or maintain the vehicle

Use public transportation and ride-sharing [outsource] - A $112B market, though the actual value is higher considering public subsidiesAt this point, the pattern should be obvious.

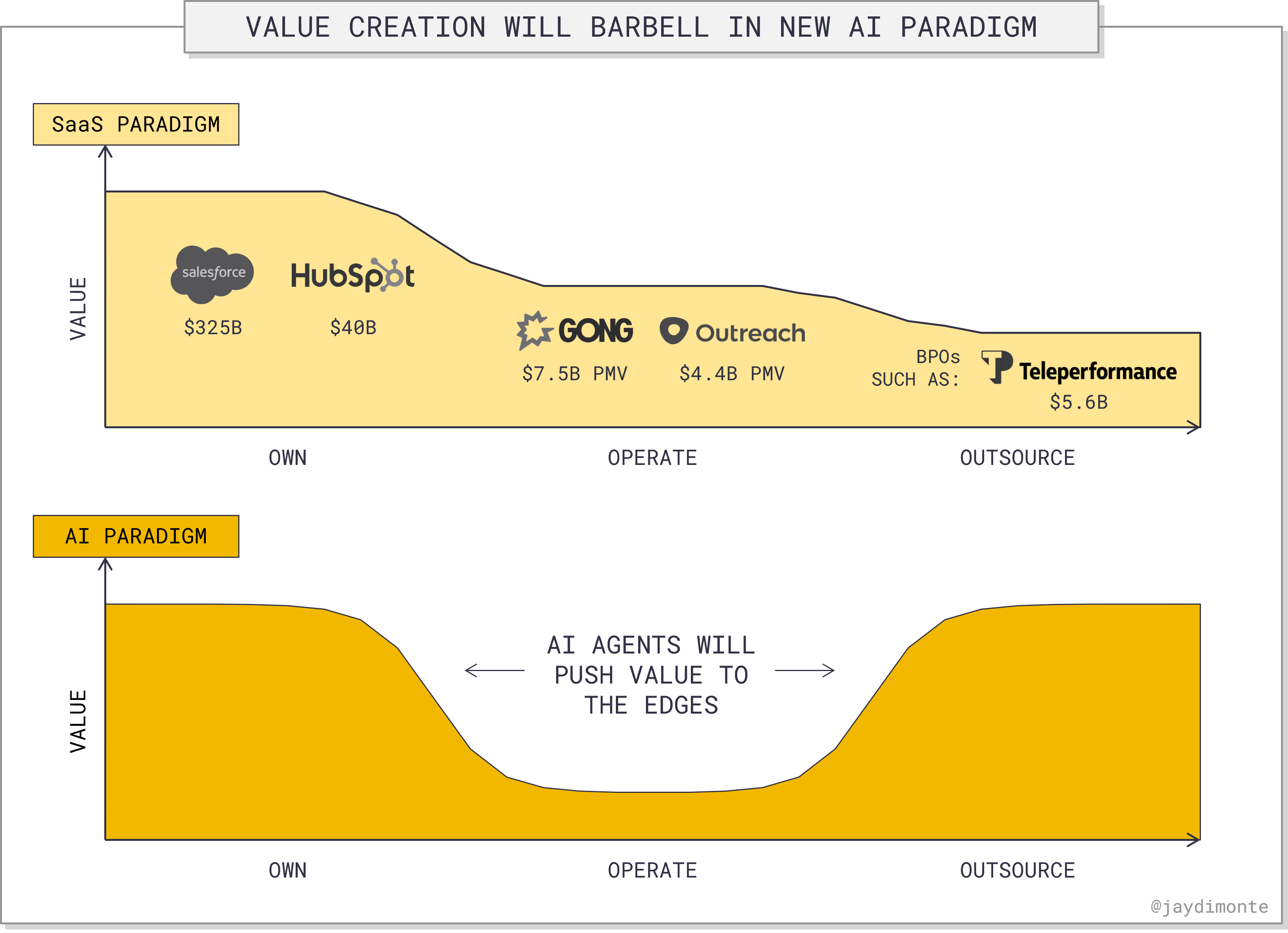

The most value accrues at the extremes—either from selling goods that let customers own the operation or selling services that allow them to outsource the function entirely. The smallest market opportunities, in aggregate, sit in the middle—where customers must still operate but do not fully control or delegate the solution.

Software will transition to this model

This is a shift from traditional software markets. Historically, the most valuable software platforms have been those that enable customers to own their data and workflows—think ERPs, CRMs, and other core systems.

In contrast, tools that operate specific workflows without being a system of record are valuable but less so. Meanwhile, service providers like BPOs, consultants, or agencies outsource functions. They tend to be lower value—both in absolute terms (harder to scale) and relative revenue multiples (lower margins).

To illustrate this in software:

If I need to manage my sales pipeline more effectively. I can use...

A CRM [own] - Salesforce and HubSpot allow me to manage customer data and set up sales workflow. These are hundred-billion-dollar companies.

Sales operations tools [operate] - Companies like Gong and Outreach sit alongside CRMs to facilitate specific functions. These are ten-billion-dollar companies.

Lead generation services [outsource] - BPOs responsible for lead generation or customer service tend to be smaller (most are private). These are billion-dollar companies.

The top chart above represents today’s software market distribution. That’s changing.

Advancements in AI do the following:

Allow platforms to innovate faster and replicate specific functionality, more.

Create further separation between those that create and maintain data and those that rely on it.

Make services companies more efficient and effective.

This will cause the value distribution of software markets to resemble other industries.

Companies in the operate category are especially vulnerable.

Software businesses in this middle tier must decide: Can they evolve into core platforms? Or should they pivot to an outsourced solution?

New startups need to be deliberate about whether they are building an own or outsource company.

Determining O-O-O models in software

There are two questions that determine which model a company has—or should have.

The first: Is there a sole party responsible for the outcome?

Consider the meal example above:

[Own] If you buy a white onion when the recipe calls for red, it’s your fault, not the grocery store’s.

[Operate] If the meal you prepare from a kit is not good, who’s fault is it? Were the ingredients bad? The recipe? How you prepared it? Who knows!

[Outsource] If there’s a rotten onion on your salad at a restaurant, it’s their fault. When it’s not clear who to blame, the solution falls in the operate category.

From a software perspective, think about bad data or integrations.

Imagine using an app that transcribes call notes and ports them to the CRM. If a call logs to the wrong customer record, why? Was the customer's phone number wrong in the CRM? Was the integration misconfigured? Did the calling app use flawed logic, and try to match a fax number instead?

When the responsibility for an error is unclear, neither party is solving the problem.

This is a vulnerable position for vendors. If the customer decided they can solve the problem better themselves, they might! If the data owner builds another module, it might make the app redundant.

The second: Is the function a competitive differentiator for our customers?

Consider transportation:

The car you drive can be more than a way to get from point A to B. It can signal something about who you are.

For example, what's the driver that comes to mind when you see a minivan? Soccer mom or dad. An F-150? Texas ;).

These stereotypes exist because vehicles serve specific and different purposes. These purposes are differentiating, be it functional or in creating an image.

Contrast that to taking public transportation. You don't care that the train car is red or blue, just that it gets you there. Unique and critical problems indicate the method of solving them is a differentiating factor for businesses. In these cases, a vendor should provide tools for customer to own their work.

If the problem is universal and not differentiating?

The product provided should solve as much of the problem as it can. Customers should feel capable to outsource the work.

This is the reason that folks search out financial advisors and tax professionals. Doing taxes is not particularly differentiating work. (Especially compared to time spent doing our own work, with family or on hobbies.) We should be happy to outsource it.

I'd argue, the only reason we don't outsource it is because of cost. If AI drives down the cost enough, hiring an accountant may become more attractive than TurboTax in the long run.

How Grid is investing in the AI Era

AI is reshaping software-as-a-service and reinvigorating service-as-software, unlocking new opportunities across both models.

These models and how they align with the problems customers are trying to solve are top of mind. Accordingly, the investments we make at Grid fall into three primary models.

First, systems that enable customers to own functions most important to them. These are platforms businesses use to design, execute, and manage core business functions. For example, ERP (enterprise resource planning), PM (project management), or other execution systems.

For example, our first investment at Grid, Scaffold, uses AI to unlock data sets that were previously inaccessible to digital solutions. The platform will become a critical tool for customers to execute their work.

Second, tech-enabled services that allow customers to outsource their problems. Vendors deliver a solution, as opposed to giving businesses a tool to better manage their problem. For example, tech-enabled staffing solutions or other AI-enabled agency work.

For example, a prior investment, Greenlite, delivers construction permits. They could have built a tool for municipalities to manage permits. They could have sold a platform for developers to organize them. Instead, they are solving a full, painful, but undifferentiating problem.

Third, networks. These solutions provide benefits driven by counterparty trust and efficiency versus specific technology. For example, marketplaces or fintech. (Though outside the scope of this particular essay, the heuristics of outsourcing apply.)

This new AI paradigm presents ample opportunity, particularly across markets represented by $1T+ of legacy industrial technology market cap. As traditional software moats erode, upstarts will have more space to maneuver. We’re eager to find and support them.

Thanks for sharing such a thoughtful perspective, Jay! Your point about deciding what to own, operate, and outsource when implementing AI perfectly resonates with what we’ve been seeing in the manufacturing sector—especially for mid-market companies. Many of these long-established factories now face a more urgent challenge because AI is redefining not just software solutions, but also core R&D and physical product development. I’ve noticed how those who leverage flexible, no-code platforms can move faster while preserving their unique brands and crafted solutions. Meanwhile, the more “traditional” players risk being outpaced by nimble startups. It’s great to see your insights line up with these real-world observations, and I look forward to reading more of your work!

Your observations on own operate and outsource are spot on. However, for the CRM industry outsource is a 50Bn+ industry where Teleperformance, Majorel and Telus kind of companies fall in and still it follows a Barbell curve.