Day by Jay #4: A tale of two markets

🎨 Sunrise 📊 Reopening will be slow and uneven 🧘♀️ Santosha and Tapas

Welcome to “Day by Jay!” A combination of topics I find interesting and enjoyable, I hope you do as well. Previous editions can be found here. Please let me know what you think @jaydimonte

🎨Art

My 2020 new year’s resolution is creating a new drawing or painting each week. Sharing here for accountability!

I love sunrises.

My morning routine has not changed in the last five or six years. I wake up, make coffee, read, and exercise. During weekends, this ritual extends late into the morning. It’s the most relaxing and consistently enjoyable part of my day.

This is a morning view from my last apartment.

📊VC & etc.

Quick takes on anything related to frameworks, startups, and VC.

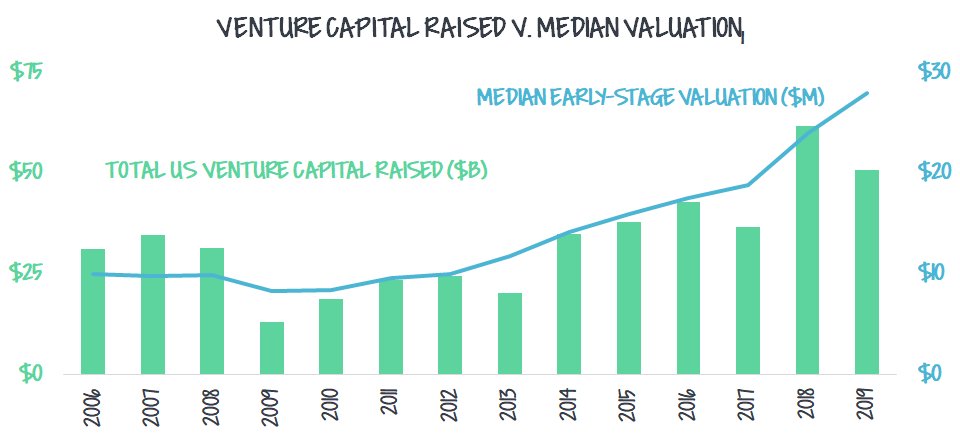

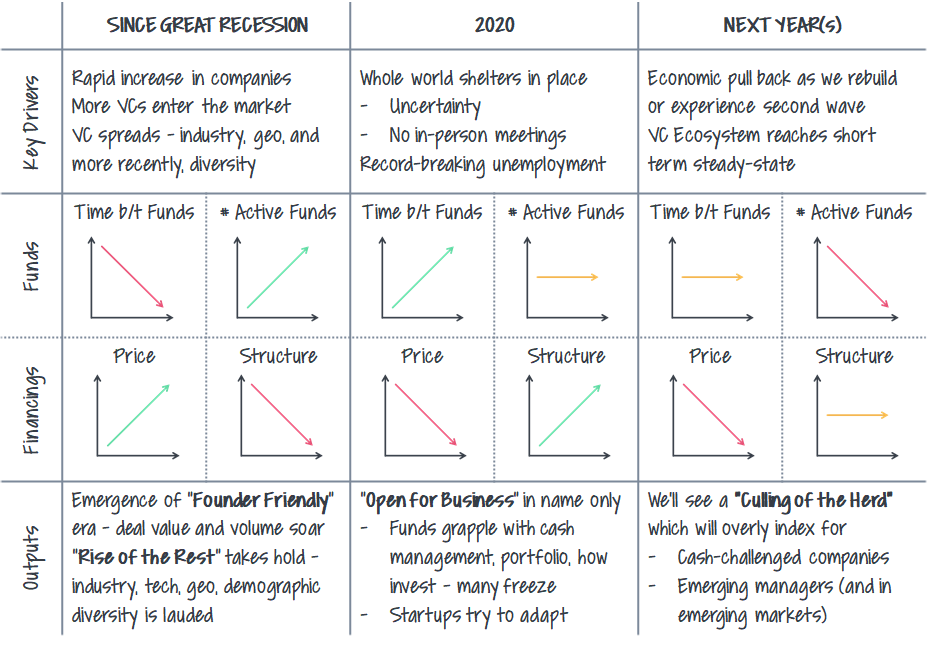

The venture ecosystem blossomed the last 10 years coming out of the Great Recession. More startups, more funds, more capital!

Then, COVID hit. We saw a dramatic pullback in VC sentiment and activity.

As the marketplace picks back up, not all VCs and the startups they fund will emerge in the same form as before. Blue-chip funds with institutional backing will feel stable and ready to resume business as usual. Younger and smaller funds stand on shaky ground.

A vibrant marketplace…

The venture-startup flywheel flourished over the last 10 years.

During the Great Recession, the number of venture capital funds and financings dropped. With almost nowhere to go but up, fund and deal closings increased in lockstep over the next five years.

The following years saw the balance tip. Though the number of venture capital funds held constant, we saw more capital raised and fewer opportunities. This was the era of "flight to quality" and "frothy markets." We saw 10-20x revenue multiples become commonplace.

In 2017, Softbank entered the market with a $100B fund, 3x the amount that all US VCs raised that year. VCs raised larger funds to compete. The new normal of mega-rounds came with lofty valuations across the board. "Founder friendly" was no longer a differentiator. The market was "hot."

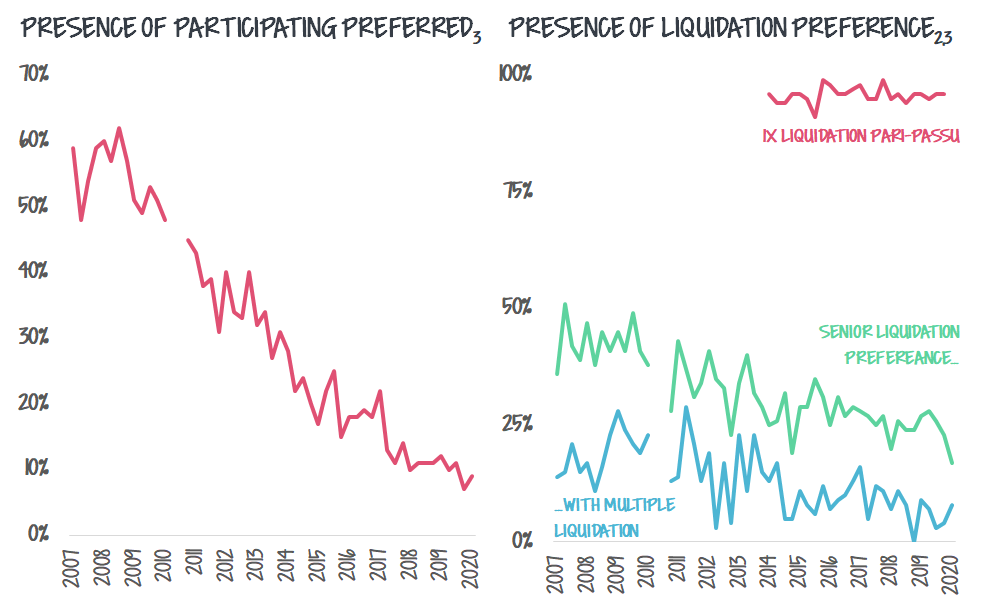

Hot markets are slick

Marketplaces excel when transactions are frictionless. That's what happened in the venture ecosystem. Term sheets and legal agreements standardized as VCs competed. Terms that were commonplace 10 years ago are now “predatory.”

A quick primer on liquidation preference and participation can found here.

Marketplaces excel when transactions are frictionless - it's why AirBnB launched instant bookings. That's what happened in the venture ecosystem. Along with the adoption of SAFEs and convertible notes, transactions became quicker, easier, and cheaper. As the barrier to funding lowered, more financings happened.

…that quickly closed

Yesterday's hot markets quickly cooled.

The combination of shelter-in-place — over 30% of VCs are unwilling to make new core investments without meeting the founder(s) in person first [4] — and economic uncertainty — of startups deep in fundraising when COVID hit, only 35% closed the round as planned, about a third closed with terms renegotiated and the remaining rounds fell apart [7] — was enough to do it.

I won't belabor the point, but you can read my thoughts, "Where did all the VCs go?"

…and are reopening slowly

The contraction of the venture ecosystem will be a result of this VC pull back. It's not that the supply of startups has dried up, its that most know this is not a good time to raise and so they aren’t.

Even as VCs come back to the marketplace, their pace will be slower. 80%+ expect to make two or fewer investments per quarter in 2020 vs. 56% in 2019. [4]

With the power shifting back to VCs for all but the hottest of companies, yesterdays' trends are likely to reverse. We'll see more entrepreneurs weigh the trade-off between valuation (down or up round?) and structure (multiple liquidation preference?). Even more so at the later stage or when companies running out of capital and bridging to exit.

A tale of two marketplaces

What about the VCs themselves not just the checks they’re writing? We need to include LPs (investors in VC funds) in this discussion.

Many LPs that curtailed their venture programs during the Great Recession regretted it. First, they missed out on the legendary funds seeding Uber, AirBnB, and others. Second, they weren't allowed back in. It's fair to expect they won't make the same "mistake" twice. So, VCs with more institutional backing (endowments, pension funds, etc.) are likely protected.

VCs backed by high-net-worth individuals and family offices may not experience the same stability. These VCs tend to be "emerging managers," newer groups that are still on their second or third fund. Any economic pull-back will disproportionately impact these groups. In fact, of those raising now, smaller funds are much more likely to modify their fund size downward. Almost half of those raising up to $50M are expecting a smaller fund than their original target. [4]

Your neighborhood VC

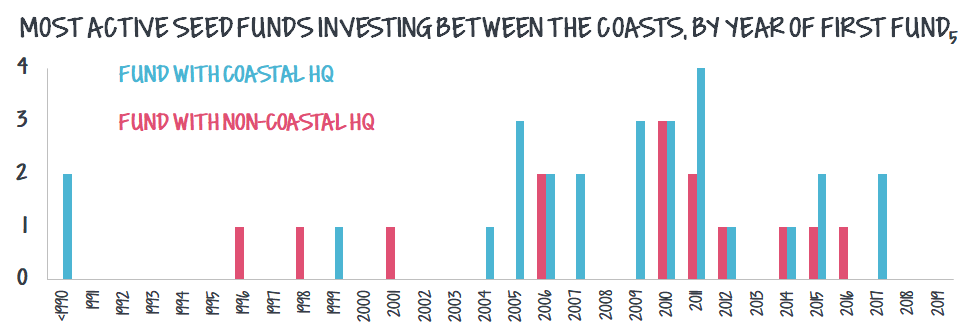

These smaller and younger funds are likely seed or pre-seed funds. Many will include non-Bay Area funds.

If you consider the most active funds investing between the coasts, a majority started after the Great Recession. Hyde Park is part of the 2011 cohort and many of our peer Chicago funds formed around the same time.

Yes, one explanation could be that there there are more funds now. If you choose any fund at random, there's a good chance it was "newly formed."

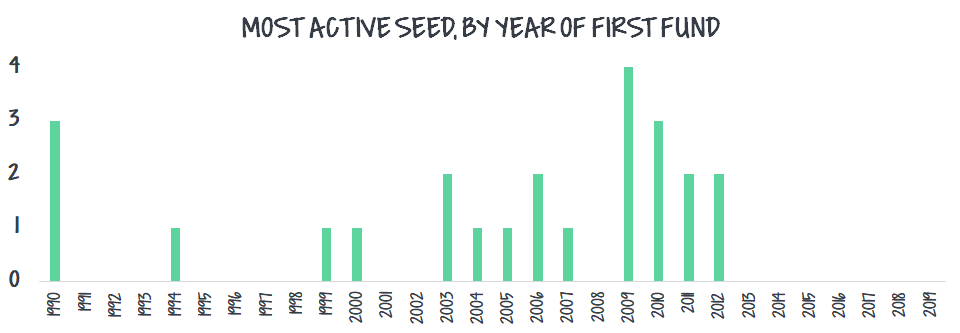

But, when you look at the most active seed funds in the US, the same pattern does not hold.

(Most of these headquarter in Silicon Valley or the East Coast. There are nine funds that overlap the two charts, including one that is HQ’d outside of the coasts, techstars.)

The median launch date for funds investing between the coasts is 2010. For all seed funds shown, 2007. This might not seem like such a large difference but it adds up to about one fund cycle. One fund can be the difference between institutional backing and not. And that backing can have a huge impact on the success of a VC’s fundraise. There is early evidence to support this. Silicon Valley funds are the least likely to decrease their fund-size target as a result of COVID. [4]

Because Hyde Park is a geographic-focused firm, we tend to see through this lens first. I'm afraid this trend will likely hold for other thesis-driven funds including those with an industry or diversity focus.

Local seed supply

Unfortunately if this plays out, some of these funds will raise less capital and others won't raise at all. Since seed investing is a local game, this will disproportionally impact non-coastal companies.

Already, there has been a divergence of seed financings over time. The difference in pre-money valuation between the top and bottom quartiles as increased.

My hypothesis is that these bottom half of valuations correlate with geography. Of course, not all companies with lower valuations are HQ’d outside the coasts. But, $10M on $90M+ Clubhouse pre-seed rounds are rarer here. After all, seed rounds in the middle of the country are 30% smaller on average than those on the coasts. [5]

Yes, seed rounds occur in local-markets. But, later-stage rounds transact in a national or global market. Midwest valuations are 50-60% lower than the Valley at the early stages. But, they grow to 80%+ of Valley prices at the Series C stage. [6]

There may even be a boost at the later stages. Our transition to shelter-in-place has changed the mindset of many. Who knows, it may be enough to entice VCs that resisted the notion that big companies could flourish between the coasts.

Reopening will be slow and uneven

All in all, we've already seen the shift from frothy and founder-friendly to a more tempered market. Yes, there will still be mega financings. Far more common, the median company will raise at a lower price. The median VC will raise less capital. Unlucky or struggling companies will raise down rounds, structured rounds, or both.

The reality is, here in the mid-continent, we're used to doing more with less. It might make us better prepared to weather the storm.

No one knows what the “new normal” will look like. It will play out in one of two ways.

In one scenario, investing becomes even more local in the very short term — I can grab a socially-distant coffee in my own city without getting on a plane — we'll need to figure out how to adjust to this new marketplace quickly so that our growth doesn't slow down.

In the other, our new comfort with distributed work fuels a wave of companies between the coasts. They will hire coastal talent, relocating to more affordable and enjoyable communities. This talent will bring coastal networks and brands, and entice coastal funds. Local seed markets will become national.

🧘♀️Deep Breath

Like yoga ends with savasana, we end here with a sense of well-being.

If you remember from the last newsletter, my yoga studio had been working through a theme each week. We focused on the yamsas (dont’s) and are now working through to the niyamas (do’s).

The second niyama is Santosha, meaning contentment, acceptance.

I’ve struggled with this one. It feels counterproductive to feel content, too “zen” for someone who likes accomplishing. It also feels at conflict with the third niyama, tapas.

Tapas is as austerity, self-discipline, perseverance, burning enthusiasm!

It reminds me of a book by reporter Dan Harris, 10% Happier. He regularly associated burnout and stress with the process of achievement. But through experience with meditation, he comes to find they don’t correlate.

I haven't tried a silent retreat (one source of Dan's breakthroughs). I have tried one method of melding santosha and tapas, the Goals vs. Systems framework... though I'm sure Scott Adams, Dilbert creator didn't have yoga in mind when he wrote about it!

Sources

Pitchbook-NVCA Venture Monitor Q1 2020

CooleyGO Venture Trends

Fenwick West Silicon Valley Venture Capital Survey Q1 2020 (and historical surveys, not linked)

Thanks for reading, please let me know what you think. Stay safe and healthy. Ciao! 👋